Interim budget take on consumption slowdown to act as cues for retail

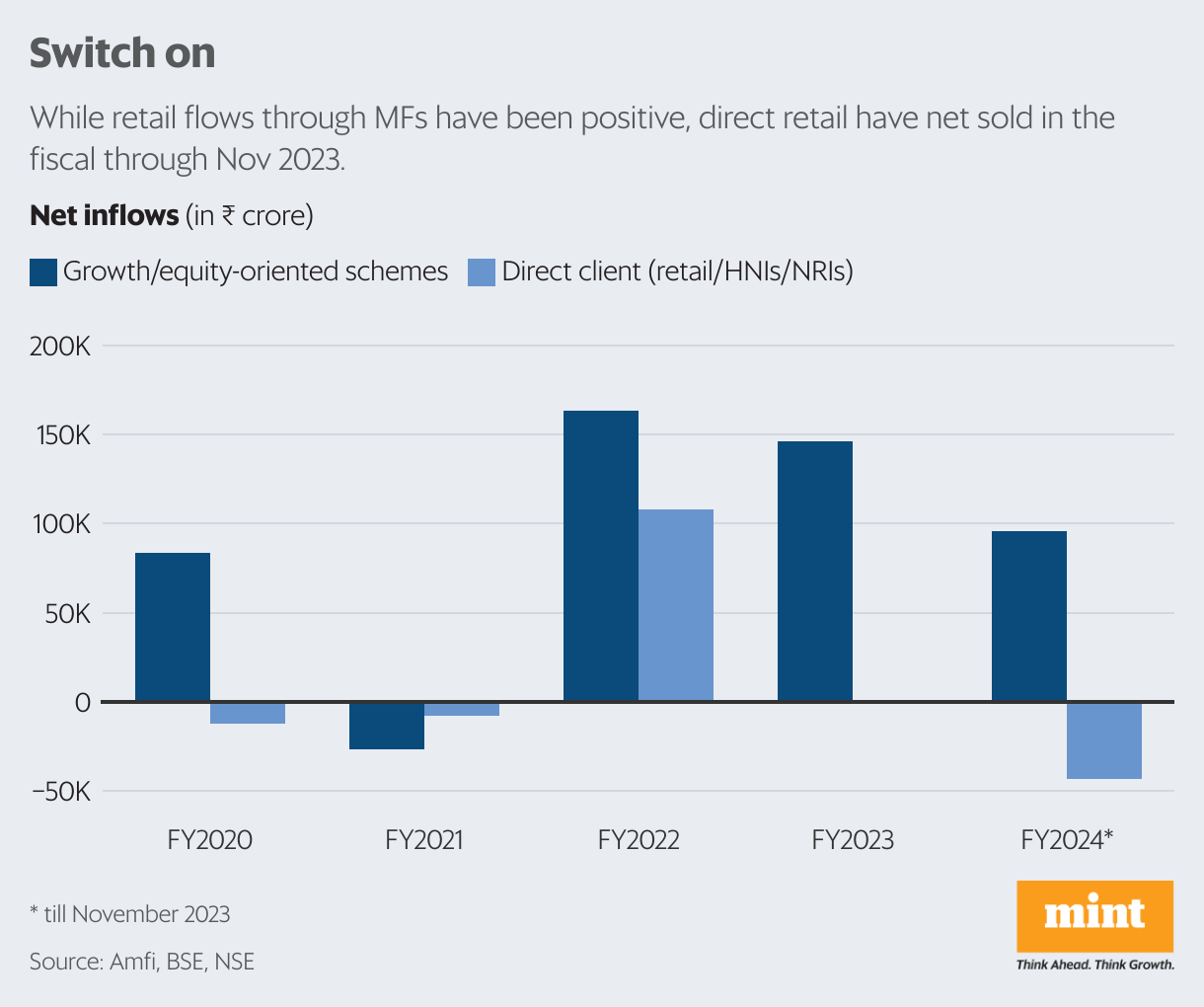

A surprising divergence has cropped up in the equities markets ahead of the interim budget wherein retail investors have been net sellers in the cash market, while those trading through mutual funds continue to invest in equity schemes.

While attributing the divergence to profit-booking by direct retail investors, market veterans believe that the interim budget is not likely to contain proposals to directly impact the market, but that finance minister Nirmala Sitharaman’s statements would be parsed carefully for measures that could address the consumption slowdown. Markets would also keenly eye statements that have a bearing on fiscal prudence.

While retail investors and high networth individuals (HNIs) have pumped in a significant portion of the ₹95,585.6 crore via equity schemes of mutual funds in the fiscal year through November, retail investors—including small, HNI and NRI investors—investing directly on the exchanges have net sold shares worth ₹43,091 crore over the same period. While purchasing a net ₹8,700 crore on NSE, they net sold shares worth ₹51,791 crore on BSE, accounting for an overall net sale figure in the period under review. “The sale in the cash market can be attributed to profit boo-king, guided by investor desire to invest in other asset classes like realty, or be purely need based,” said Vijay Mehta, president of nodal brokers body, Association of National Exch-anges Members of India, or ANMI.

Motilal Oswal’s head of retail research Siddhartha Khemka agreed and added that as the selling was on BSE it would have been related to “profit booking in mid-, small- and micro caps.”

While NSE data on retail investor flows in December will be released with a lag, BSE data shows that clients and NRIs sold ₹11,221 crore of shares on the exchange.

According to market experts like A. Balasubramanian , MD & CEO, Aditya Birla Sun Life AMC, statements of the government intent to address the consumption slowdown “could fuel” fresh retail flows into equities.

“One way to address the slowdown could be by putting more money in the hands of taxpayers by relaxing personal income tax slabs. That won’t happen in the vote on account, but statements acknowledging the need to address the consu-mption slowdown could possibly drive retail flows into markets,” said Balasubramanian.

While the NSO’s first adva-nce national income estimates peg the Indian economy’s real GDP growth at 7.3% in FY24—making it among the fastest -growing world economies—private financial consumption expenditure (incurred by resident households and non profit institutions serving households on final consumption of goods and services) is expected to grow just 4.4%, the slowest in the past two decades barring the pandemic hit FY21.

According to Nilesh Shah, MD, Kotak Mahindra AMC, “This being a vote on account is unlikely to have any proposal to change tax rules to encourage retail participation in Mutual Funds or Direct Equity. However the guidance in the vote on account on the path of fiscal prudence will undoubtedly be watched by the market.”

The interim budget is expected to forecast fiscal deficit , the difference between government expenditure and income, at 5.3% for FY25 against estimated 5.9% of GDP for the current FY.

Markets like a contained deficit as this keeps a check on the cost of money as the governments usually tend to borrow more to fund the deficit , which has a bearing on interest rates.

Ganesh

http://ganesh@finplay.inFinance enthusiast, Mutual fund expert.