Keep expectations low from Page Industries

Patience is a virtue, but that may not be the case if you are an investor in Page Industries Ltd’s stock. This is because the wait for an earnings turnaround is getting longer. Weak demand, heightened competition and an inferior product mix is feared to keep its realizations muted in the March quarter (Q4FY24) as well as FY25.

Declining cotton prices have prompted competitors to give discounts and unwind inventory. But Page’s firm realizations indicate it isn’t following suit yet and this can be a problem. Page generally stays away from discounting, but persistent high levels of inventory (+70 days) in the market may force it to either face more volume pressures or may result in price cuts, thereby impacting realizations, said an Kotak Institutional Equities report dated 26 March.

Page holds the exclusive license for the manufacture, marketing and distribution of the Jockey brand in some countries including India. It also holds the sole license of the Speedo brand in India. “Page’s performance in Q4FY24 is likely to be muted with subdued revenue growth,” said Varun Singh, analyst at ICICI Securities, adding that athleisure remains a pain point for Page, contributing more than 30% to revenues

Recall that in Q3, Page’s revenue grew marginally by 2.4% year-on-year, after remaining flat to negative in the previous four quarters. Volume growth of about 5% was driven by the innerwear segment, while athleisure wear continued to be a laggard. Now, if the core issue of excessive inventory persists in the athleisure segment, it could delay a meaningful earnings recovery.

In this backdrop, from Q4 management commentary, investors will watch out for the overall industry demand scenario, how the company’s software implementation is panning out and whether inventory-led issues have bottomed out.

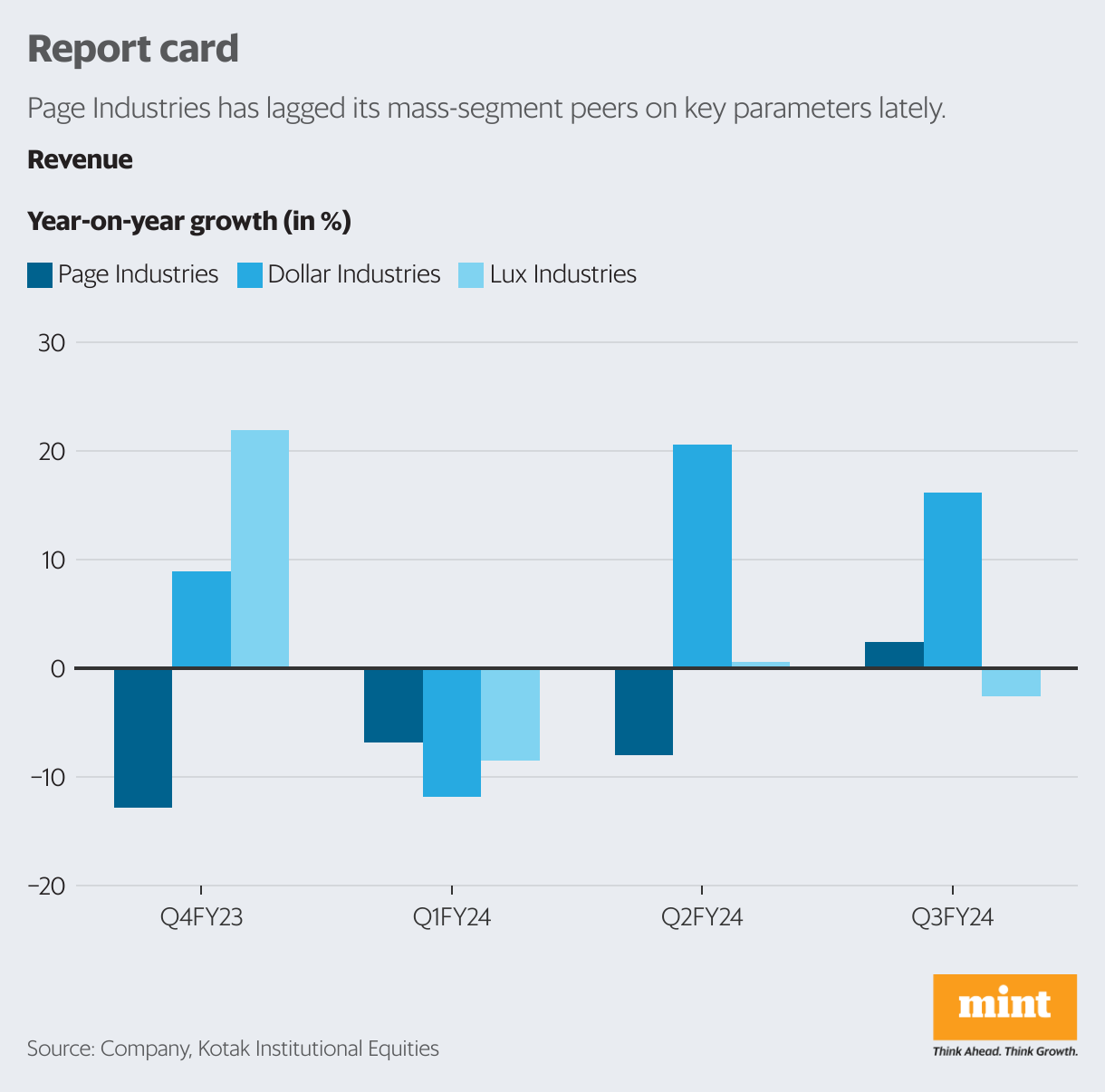

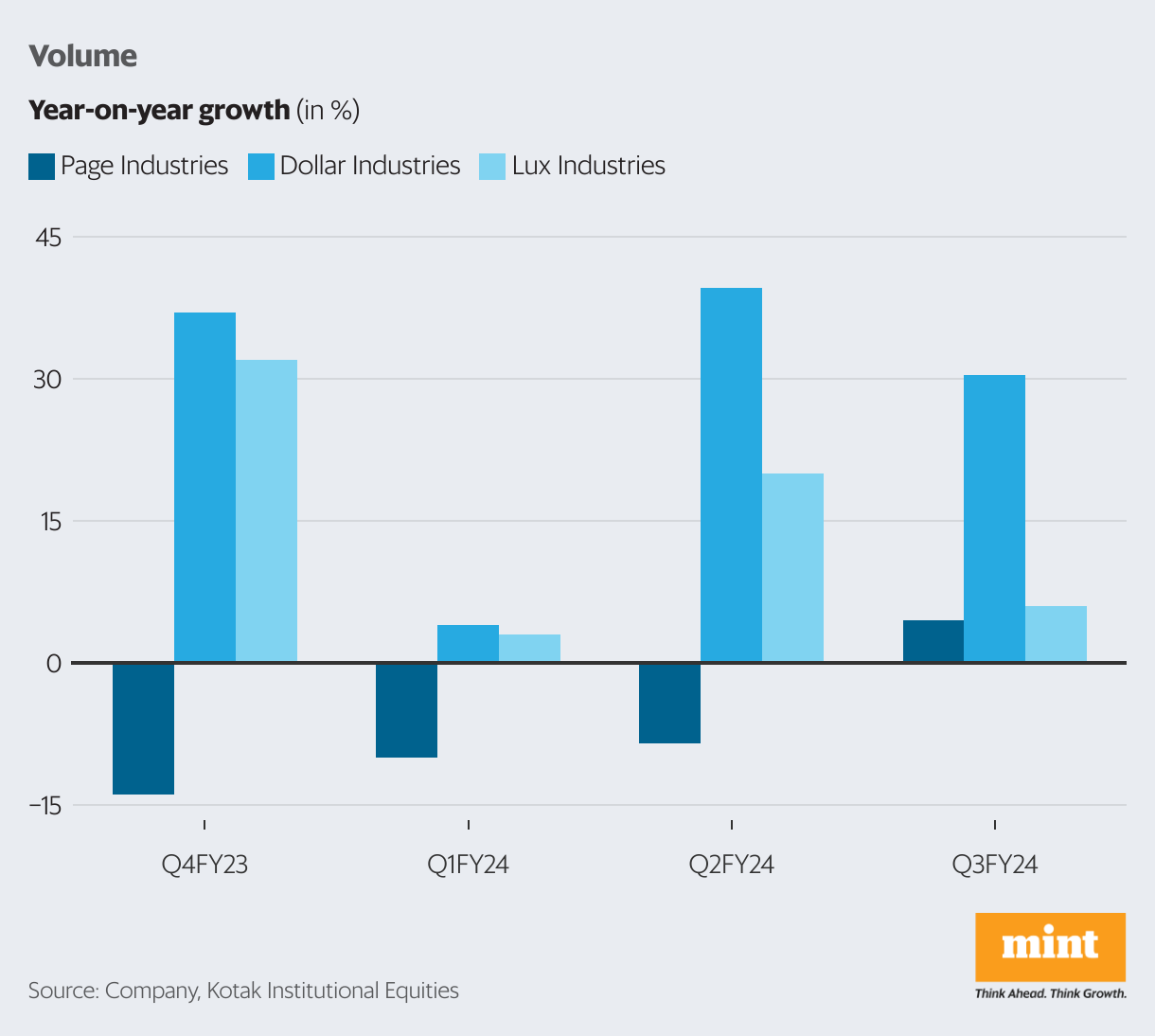

Page’s recent earnings performance suggests it is feeling more pressure of the overall weakness in consumption demand for innerwear products than those having exposure to the mass segment. Note that there is no like-to-like comparison between Page, Dollar Industries Ltd and Lux Industries Ltd as the other two companies offer innerwear products at relatively lower price points. As the chart alongside shows, revenues of other value-focused listed peers such as Dollar and Lux have grown faster than Page in the recent four quarters. This is attributed to entry-price products witnessing better demand than Page’s products. This could be a fallout of consumers opting to down-trade amid muted demand. As such, Page is not looking to tweak prices any time soon.

In other words, the levers of favourable product mix and price hikes, which fuelled Page’s realization growth in the past, are likely fading in FY25, leaving room for further earnings downgrades.

The stock’s dismal performance signals the nervousness of investors. On 20 March, Page’s shares slid to a new 52-week low of ₹33,070.05. So far in 2024, the stock has declined by 11%, lagging Nifty50’s gain of about 3%.

Owing to the lacklustre earnings, Page’s valuations have cooled-off from the peak of over 70 times seen in the past. The stock now trades at FY25 price-to-earnings (P/E) multiple of 52 times, according to Bloomberg data.

While the company’s cost control measures are positive, the road isn’t smooth in the near-term. Its athleisure segment which benefited during covid, needs to make a comeback. Hereon, a crucial re-rating factor for Page would be the initiatives to increase channel presence via more exclusive brand outlets (EBOs) and higher online exposure. In the Q3FY24 earnings call, the management had said that there was closure of non-traditional outlets opened during the pandemic, but it continues to focus on expansion and is on track to open 150-200 EBOs in FY24, as it had guided earlier.

Athleisure, a combination of athletic and leisure, is a style of clothing that is suitable for sports but is also fashionable. The usage increased during the pandemic.

Still, investors may not allocate brownie points soon. “While valuations seem to be at a reasonable level, the stock is unlikely to perform for the next two-three quarters as we don’t see meaningful upside triggers,” says Singh.

Ganesh

http://ganesh@finplay.inFinance enthusiast, Mutual fund expert.