The one bright star in a bleak year for IT

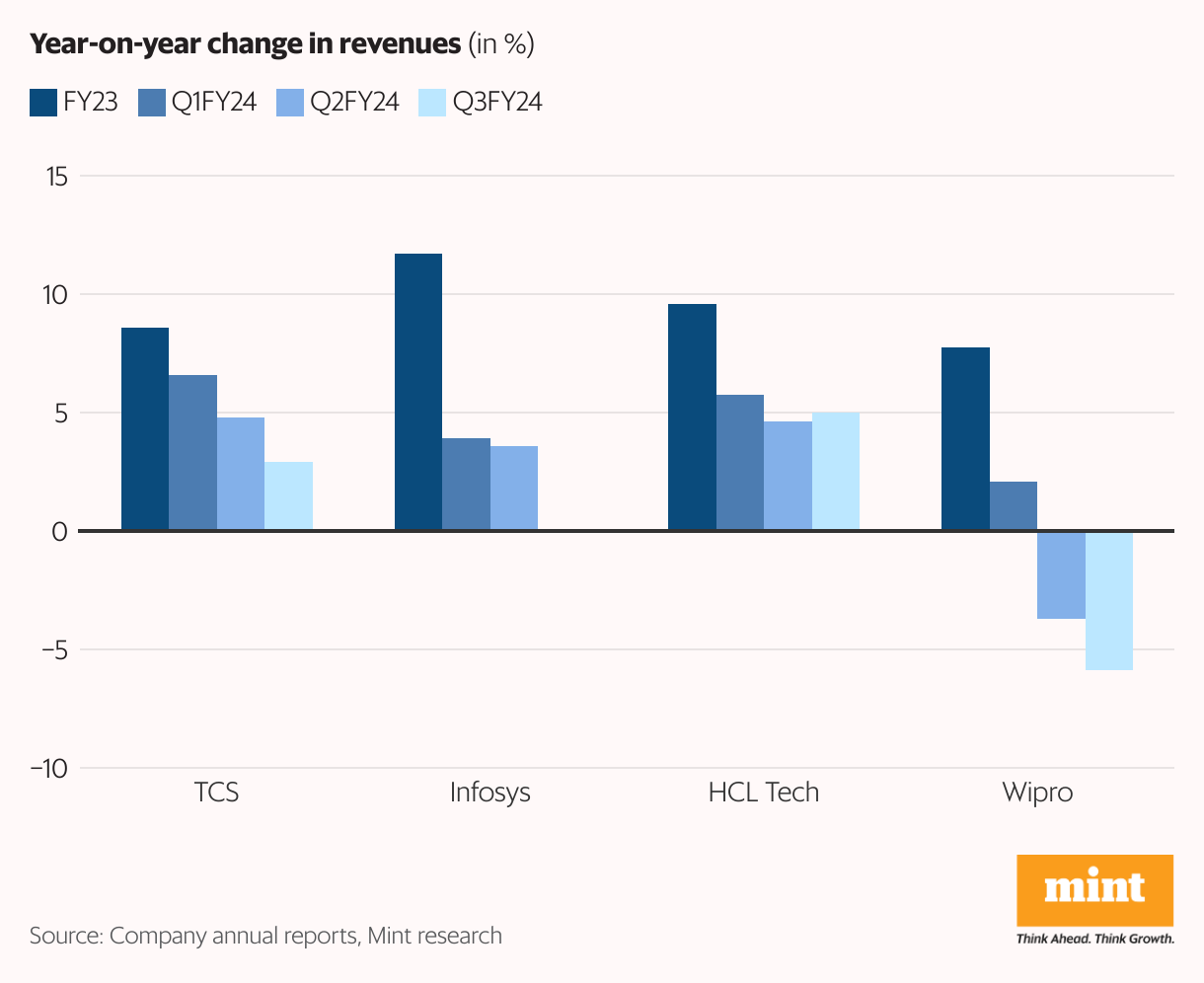

An analysis of two investor notes by financial services firms Nomura and HDFC Securities, plus a Bloomberg poll of analysts, showed the Noida-headquartered company may grow revenues by 4.7% in FY24, the best by a large-cap firm in India’s $253-billion IT services industry.

In comparison, Tata Consultancy Services (TCS), India’s largest IT services firm by market value, could end the year with a slightly slower revenue growth of close to 4%, driven by what Nomura and HDFC Securities project could be a 1.5% sequential growth in dollar revenue in the March quarter. TCS’s revenue growth in the quarter could be driven by a digital transformation deal it won from state-run telecom operator Bharat Sanchar Nigam Ltd.

Meanwhile, Infosys, the second-largest in the IT industry, may report a marginal decline in revenue in the March quarter, and 2% year-on-year increase in FY24. Wipro, meanwhile, would be the only one among the top four Indian IT firms to see a decline, with a flat March quarter projected to lead to 3.7-4.1% lower FY24 revenue.

HCL is expected to be the best performer among the top four, while others are projected to post either flat revenue for the quarter ended 31 March, or report sequential declines. TCS is expected to kick off the FY24 annual earnings season next week, when it announces its results on 12 April. Infosys, Wipro and HCL report earnings on 18, 19 and 26 April, respectively.

Analysts said the IT sector’s overall tepid performance could be attributed to the delay in discretionary tech spending. Abhishek Bhandari, executive director of equity research at Nomura, said the IT services industry presently has no signs of discretionary demand revival. “Indian IT services companies are likely to see some respite from weak seasonality and furloughs of the December quarter (of FY24). However, in the absence of a firm recovery in discretionary demand, growth recovery in Q4FY24, and FY25, should be led primarily by cost-takeout projects… suggesting the current slowdown’s impact extending into FY25 discretionary spends,” Bhandari said. He also expressed caution on the industry’s near-term growth prospects due to “limited visibility on a significant turnaround in discretionary demand.”

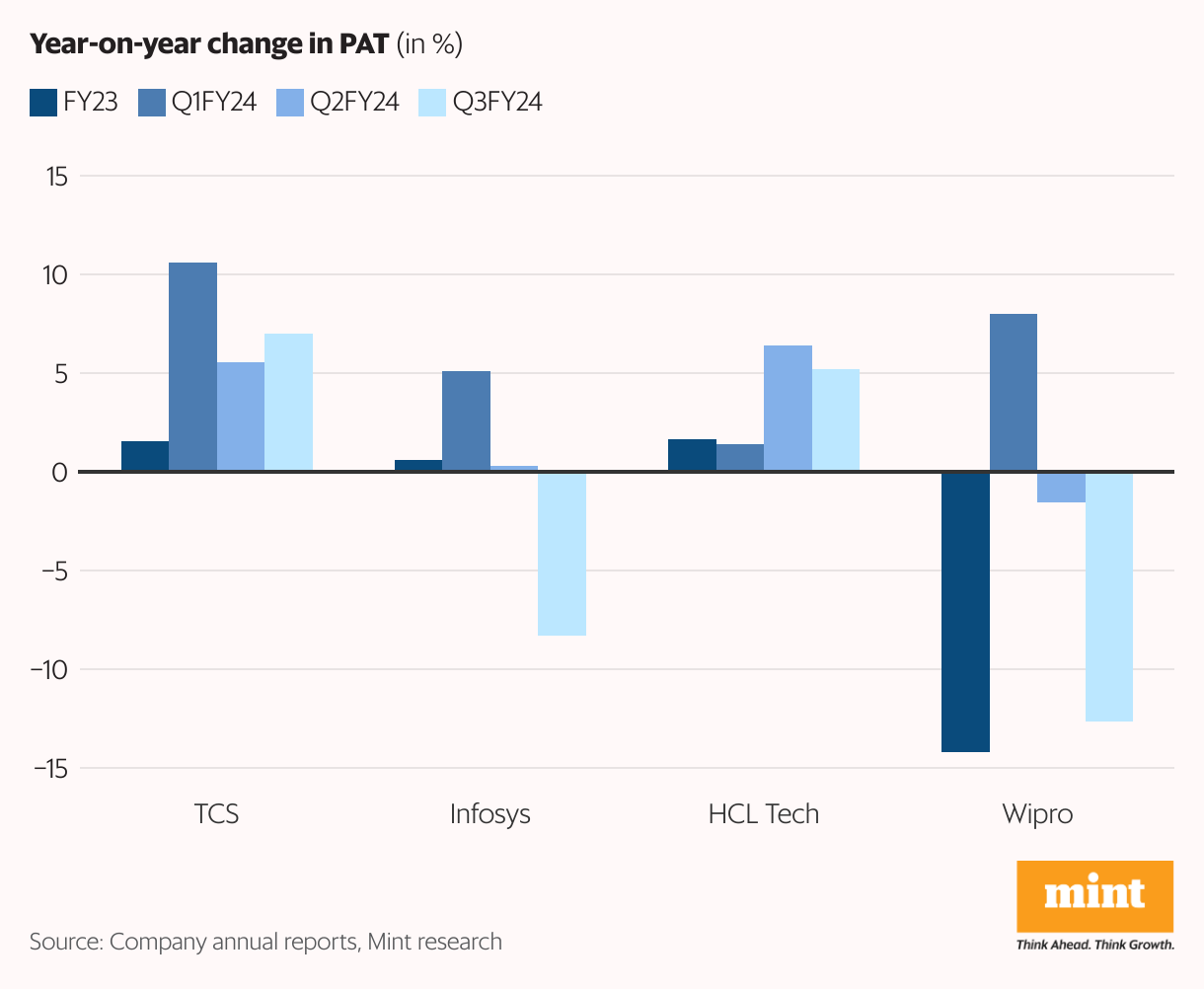

A Bloomberg poll of 43 analysts projected TCS to report FY24 revenue of $28.97 billion, thus registering a March quarter revenue of $7.26 billion—a marginal sequential decline. Net profit, however, is expected to grow 6% y-o-y to $5.53 billion, per Bloomberg analysis.

For Infosys, a poll of 38 analysts projected 1.7% annualized revenue growth to $18.52 billion, although net profit could take a marginal hit to $2.95 billion. March quarter revenue for Infosys could thus see a 3% sequential decline. For HCL, Bloomberg estimates 4.7% revenue growth to $13.2 billion for FY24, while net profit is projected to rise 3.3% to $1.9 billion. This leaves projected quarterly revenue at $3.36 billion—a 1.8% potential sequential decline, but still up substantially from FY23’s March quarter.

Wipro, as per 38 analysts polled by Bloomberg, is projected to report $10.77 billion in annual revenue for FY24, and $2.62 billion in March quarter. This translates to a 4% possible sequential revenue decline for Wipro, in what has been a year to forget for the company. Net profit, as per 39 analysts, could decline 4% y-o-y to $1.32 billion.

Chirajeet Sengupta, managing partner at financial research and consultancy firm Everest Group, concurred, adding there have been “no signs of recovery that the industry has seen through the last three months of FY24.”

Apurva Prasad, vice-president of institutional research at HDFC Securities, said in the investor note that growth in the industry, in the March quarter, “is expected to bottom out.”

“Growth will recover ‘gradually’ in FY25. The slowdown in macro is still a baseline scenario, and lower discretionary spending and slower conversion from total contracted value (i.e. the value of deals signed by these companies) to revenue is a feature and not a bug—at least in the near term. Deals will thus be focused on cost optimization,” Prasad’s note said.

For the top IT services firms, converting deals to billable projects has been a challenge. While companies have signed a large number of deals, most of them, as per industry executives, are deferred in terms of their billing cycles. For clients, many prefer delaying a signed-on tech project—which is often a sign of macroeconomic concern and sectoral weakness.

Everest’s Sengupta said that recovery is likely to be slow. “We do expect the second half of this calendar year to show some signs of recovery, part of which would be driven by a base effect of the decline in discretionary deals, which started from around mid-calendar year 2023. Beyond a point, there’s only so much that one can delay tech spending, and digitalization is a crucial factor for pretty much all companies—making such spends less discretionary in nature,” he said.

However, he also warned about weak prevalent macroeconomic conditions around global geographies. “Over the past few weeks, macroeconomic signals do not seem to be picking up as positively as one would have hoped. Inflation is proving to be slightly more stubborn than what one had expected, and quite a few economies are going into recession. It will therefore be a slow recovery, and there definitely won’t be a U-shaped recovery that we had previously expected.”

(With inputs from Mayur Bhalerao)

Ganesh

http://ganesh@finplay.inFinance enthusiast, Mutual fund expert.